Major Life Events & Estate Planning—When to Update Your Documents

Apr 24, 2025Marriage, divorce, new children, big windfalls—learn when and why to update your estate plan so it always reflects your life’s changes.

Table of Contents

- Introduction

- Why Updating Your Estate Plan Matters

- Life Events That Trigger Updates

- Key Documents to Revisit

- Common Mistakes & How to Avoid Them

- Practical Steps to Keep Your Plan Current

- Estate Plan Update Checklist

- Additional Resources & Next Steps

- Relevant Government Links

- Conclusion & Disclaimer

1. Introduction

Estate planning is not a “set it and forget it” endeavor.

As your life evolves—through marriage, divorce, births, deaths, career changes, and more—your estate plan should evolve, too.

Otherwise, you risk outdated instructions, unintended beneficiaries, and needless complications for your loved ones.

In this post, we’ll discuss why timely updates matter, which life events should prompt a review of your estate documents, and practical steps to ensure your will, trusts, and beneficiary designations remain aligned with your current situation and wishes.

If you’re new to estate planning, check out the blog on Estate Planning Basics for an introductory overview.

2. Why Updating Your Estate Plan Matters

2.1 Reflecting Current Wishes & Circumstances

- Family structures shift. A will written before you had kids or after a divorce may be outdated.

- Financial circumstances change. You might gain or lose assets, inherit property, or start a business.

2.2 Avoiding Legal Confusion

- Conflicts may arise if an ex-spouse is still listed as a beneficiary on your life insurance or if a deceased loved one remains an executor of your will.

2.3 Protecting Loved Ones

- Ensure your estate plan keeps pace with your dependents’ needs, especially if you have minor children or someone with special needs who requires ongoing care or trust management.

3. Life Events That Trigger Updates

3.1 Marriage or Remarriage

- Combining assets: Decide whether to keep property separate or jointly titled.

- Beneficiary changes: Update wills, trusts, retirement accounts, and insurance policies to include your new spouse.

- Blended families: If you bring children from a previous marriage, clarify how assets will be divided.

3.2 Divorce or Separation

- If you don’t remove or adjust your ex-spouse’s standing in your estate documents, they may remain a default beneficiary.

- Certain jurisdictions automatically invalidate some provisions after divorce, but not always. Double-check your local laws.

3.3 Birth or Adoption of a Child

- Name a legal guardian in your will for minor children.

- Consider setting up or updating a trust to manage your child's funds until they reach adulthood.

- Adjust life insurance or retirement plan beneficiaries to include or account for your new child.

3.4 Death of a Loved One

- If an executor, trustee, or beneficiary passes away, you need to reassign roles or reallocate assets.

- Failing to update can lead to confusion or more complex probate if your intended representative is no longer living.

3.5 Significant Financial Changes

- Windfalls: Large inheritances, lottery wins, or significant business successes can significantly impact your tax liabilities and distribution strategies.

- Job changes: A new job with different benefits or stock options might warrant a beneficiary update.

- Business ownership: If you acquire or sell a business, review your estate plan to ensure it addresses any new or missing provisions.

3.6 Relocation or Moving Abroad

- Different jurisdictions, such as states or countries, may have unique rules regarding community property, estate taxes, or probate.

- If you move internationally, you might need separate wills (one for each country) or revise them to comply with local inheritance laws.

3.7 Health Changes or Retirement

- If you’re diagnosed with a chronic or terminal illness, revisit your healthcare directives and Power of Attorney (POA).

- Retirement often changes your financial structure—you may consolidate or move accounts, requiring new beneficiary designations.

4. Key Documents to Revisit

4.1 Last Will and Testament

- Update who inherits, who serves as executor, and guardianship for minors if circumstances shift.

- Align the will with any changes in trusts, property titles, or beneficiary forms.

4.2 Trusts

- Revocable living trusts can be amended to account for new children, spouses, or changes in your asset portfolio.

- Specialized trusts, such as special needs trusts or charitable trusts, may require adjustments if your beneficiary’s condition or your philanthropic goals change.

4.3 Beneficiary Designations

- Retirement accounts, life insurance policies, and bank accounts (POD/TOD).

- Updating these forms is crucial; they often override will provisions if they conflict.

4.4 Power of Attorney (POA) & Healthcare Directives

- If your designated agent moves far away, becomes incapacitated, or you lose trust in them, revise your POA.

- Review your living will or healthcare proxy to ensure it accurately reflects your current medical wishes.

4.5 Life Insurance Policies & Annuities

- Review your coverage amounts regularly to ensure they align with your family's current needs and any significant financial changes you may experience.

- Update beneficiary details to prevent an ex-spouse or the wrong person from receiving benefits.

5. Common Mistakes & How to Avoid Them

5.1 Ignoring Life’s Minor Changes

- Some people assume small changes (like moving to a new city or selling a minor asset) don’t matter, but they can accumulate and cause confusion.

5.2 Forgetting to Update All Documents

- Changing your will without also changing your beneficiary designations (or vice versa) can lead to conflicts. Ensure all documents are in sync.

5.3 Overlooking Digital Assets

- Email accounts, cloud storage, cryptocurrencies, or social media—especially if you relocate or see changes in these digital properties.

5.4 Delaying Too Long

- If tragedy strikes before you revise your documents, your outdated plan remains in effect, potentially leading to disputes or unintended consequences.

6. Practical Steps to Keep Your Plan Current

- Annual or Biannual Reviews

- Commit to an estate plan review every 1–2 years, even if no significant changes occurred, to catch minor discrepancies.

- Check Beneficiary Forms

- Quick phone calls or website logins to verify who’s listed, particularly for IRAs, 401(k)s, Superannuation, and life insurance.

- Maintain a Master File

- Keep a secure but easily accessible folder (physical or digital) containing your will, power of attorney (POA), trust documents, real estate deeds, and a list of accounts.

- Communicate

- If you decide to remove or change a trustee, executor, or guardian, let them (and relevant family members) know.

- Professional Guidance

- Consult an attorney when big life changes occur, especially after major financial shifts or relocation, to ensure compliance with local laws.

7. Estate Plan Update Checklist

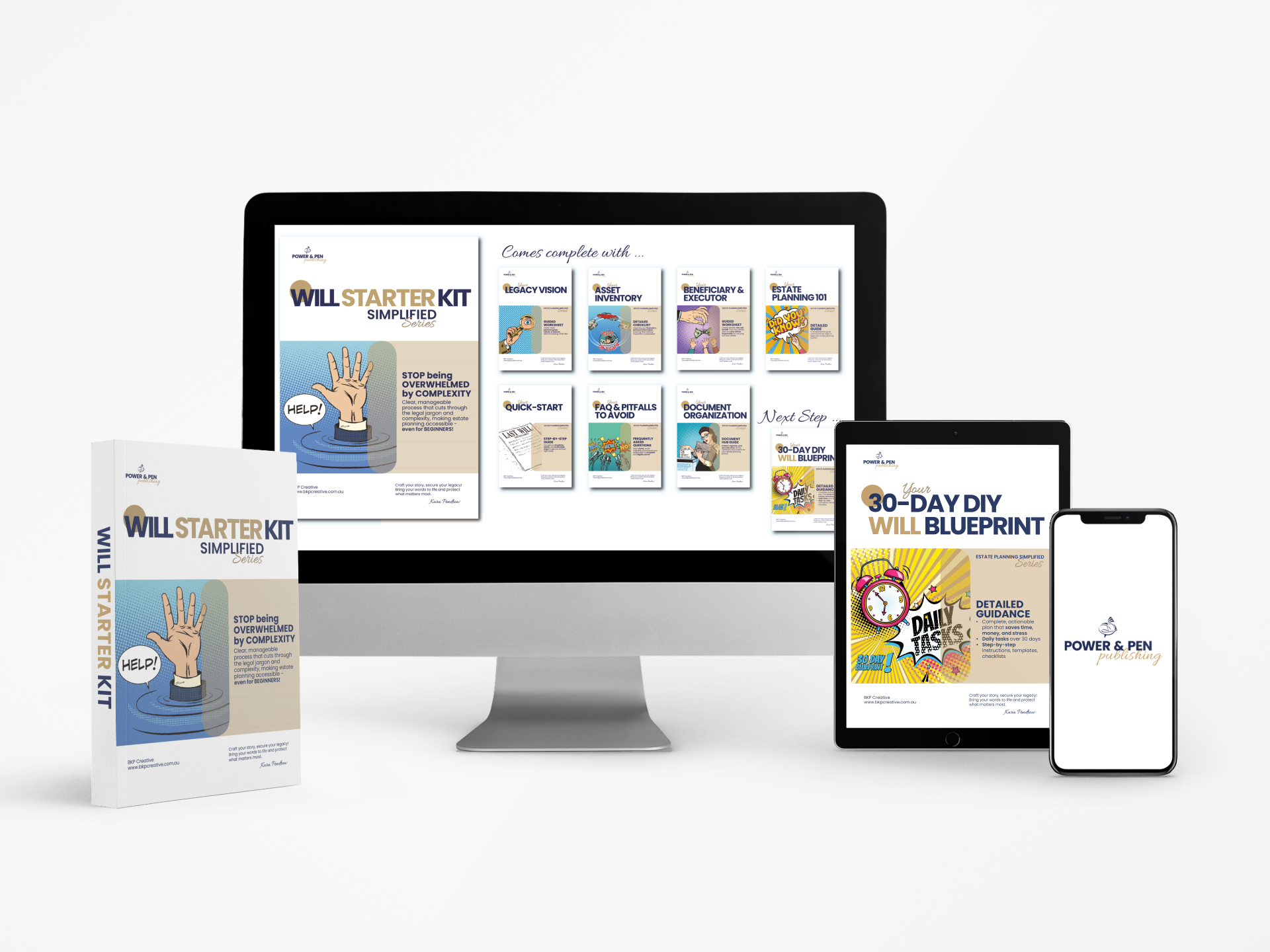

Need a simple way to keep track of all the documents that need a refresh? Our FREE Estate Plan Update Checklist is a BONUS resource in the free Will Starter Kit.

It helps you:

- Identify the triggers that necessitate an update (e.g., marriage, divorce, new child).

- List the documents (will, trust, POA, beneficiary designations) and what to check.

- Track the date of the last revision for each item.

- Ensure your estate plan remains consistent, clear, and in line with your present life circumstances.

Download the free Will Starter Kit that contains the Estate Plan Update Checklist: Your Guide to Staying Current.

This user-friendly checklist guides you through every aspect of your estate documents, enabling you to complete tasks and maintain a fully up-to-date plan with ease.

8. Additional Resources & Next Steps

- Regular Reviews: Mark your calendar for an annual review of your estate plan, just as you do with your insurance policies.

- Consult Professionals: For major life events, such as inheritances, marriage, or business ownership, consider consulting an estate planning attorney.

- Family Communication: If changes affect your heirs (e.g., new guardians or different distributions), be transparent and open with them. Visit our blog, Navigating Family Dynamics, for communication tips.

9. Relevant Links

-

Because estate laws vary by jurisdiction, here are official links to help you explore further:

United States

United Kingdom

Australia:

Canada:

New Zealand:

These resources provide country-specific guidance and up-to-date legal requirements.

10. Conclusion & Disclaimer

Your estate plan should be as dynamic as your life.

When major milestones occur—whether joyous (like a wedding or new baby) or challenging (like a divorce or death)—make sure your will, trusts, and beneficiary designations reflect today’s reality.

Disclaimer: This blog offers general educational information and does not constitute legal advice.

Always consult a qualified estate planning attorney for personalized guidance, especially when major life events arise.

Next Steps:

- Download our free Will Starter Kit

- Upgrade to Next Steps: if you need daily support, consider the 30-Day DIY Will Blueprint

- Stay tuned for more insights in our Estate Planning Series to keep your documents up to date and your legacy secure.

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.